They simply debit cash and credit accounts receivable for the full amount. Revenues are what businesses earn through selling their products to their customers while expenses are what businesses spend in the course of running their the contra account purchases discount has a normal debit balance. operations. For most businesses, the sales revenue that comes from their main operation is the main source of their revenues. Net sales revenue is equal to gross sales revenue minus sales discounts, returns and allowances.

What are sales allowances?

- An estimate of bad debts is made to ensure the balance in the Accounts Receivable account represents the real value of the account.

- Next, let’s assume that the corporation focuses on the bad debts expense.

- Instead of focusing on the fear and anger, she started her accounting and consulting firm.

- Gross sales revenue is calculated as being equal to the number of products sold multiplied by the price at which they are sold.

The purpose of the Accumulated Depreciation account is to track the reduction in the value of the asset while preserving the historical cost of the asset.

Inventory: Discounts

When the amount recorded in the contra revenue accounts is subtracted from the amount of gross revenue, it equals the net revenue of a company. In case a customer returns a product, the company will record the financial activity under the sales return account. The use of contra accounts ensures the accuracy of financial accounting records, as the value of the original accounts is not directly reduced. In the event that a contra account is not utilized, it can become increasingly troublesome to determine historical costs, which makes tax preparation time-consuming and difficult. The balance in the allowance for doubtful accounts is used to find out the dollar value of the current accounts receivable balance that is deemed uncollectible.

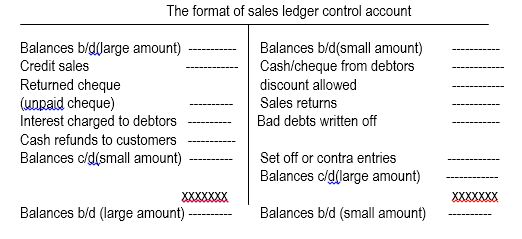

Chapter 14 – Control Accounts

Instead of focusing on the fear and anger, she started her accounting and consulting firm. In the last 10 years, she has worked with clients all over the country and now sees her diagnosis as an opportunity that opened doors to a fulfilling life. Kristin is also the creator of Accounting In Focus, a website for students taking accounting courses. Since 2014, she has helped over one million students succeed in their accounting classes.

Therefore, the amount of cash needed to fulfill the obligation is $4,850. If it estimates that $10,000 of merchandise will be returned, then its net revenue will be $90,000 ($100,000-$10,000). The company must publish its financial information at the end of the month or quarterly–far sooner than ninety days. The company will estimate its sales returns and then establish an allowance for returns.

The allowance method of accounting enables a company to determine the amount reasonable to be recorded in the contra account. When recording assets, the difference between the asset’s account balance and the contra account balance is the book value of the asset. A contra asset is paired with an asset account to reduce the value of the account without changing the historical value of the asset. Examples of contra assets include Accumulated Depreciation and Allowance for Doubtful Accounts. Unlike an asset which has a normal debit balance, a contra asset has a normal credit balance because it works opposite of the main account. Purchase Discounts, Returns and Allowances are contra expense accounts that carry a credit balance, which is contrary to the normal debit balance of regular expense accounts.

When you create an allowance for doubtful accounts, you must record the amount on your business balance sheet. The balance sheet is a financial statement that looks at your company’s assets, liabilities, and equity. A purchase discount is a small percentage discount a company offers to a buyer to induce early payment of goods sold on account.

Purchase discount is an offer from the supplier to the purchaser, to reduce the payment amount if the payment is made within a certain period of time. Accumulated Depreciation is a contra asset account with a credit balance that reduces the normal debit balance of Property, Plant and Equipment fixed assets in order to present the net value of long-term capital assets on a company’s balance sheet. Under the allowance method, a company records an adjusting entry at the end of each accounting period for the amount of the losses it anticipates as the result of extending credit to its customers. The entry will involve the operating expense account Bad Debts Expense and the contra-asset account Allowance for Doubtful Accounts. Later, when a specific account receivable is actually written off as uncollectible, the company debits Allowance for Doubtful Accounts and credits Accounts Receivable.

This is just one of several common allowance accounts used in accounting. This allows more consumers to purchase goods using the seller as a short-term financing option. An allowance is a contra- account with a balance opposite to the account it is linked to and is reported as a deduction to that account. The allowance is established and replenished through a provision, an estimated expense. Two typical examples of an allowance are the allowance for doubtful accounts and the allowance for returns and discounts. The purpose of a contra expense account is to record a reduction in an expense without changing the balance in the main account.

Accountants must make specific journal entries to record purchase discounts. When a buyer pays the bill within the discount period, accountants debit cash and credit accounts receivable. Another part of the entry debits purchase discounts and credits accounts receivable for the discount taken by the buyer. If the buyer does not take the discount, then accountants do not make the second entry. Gross sales is the total unadjusted income your business earned during a set time period. This figure includes all cash, credit card, debit card and trade credit sales before deducting sales discounts and the amounts for merchandise discounts and allowances.